Newsletter 135 – 05.30.2022

The 2021/22 season was not simple at all for blueberry producers and exporters in the southern hemisphere. This time the culprit was not the weather, which turned out to be correct for most countries. The complications arose mainly from logistics, which in the case of a fruit as perishable as blueberries, is a more than fundamental point. In the process that goes from the crops to the supermarket shelves, everything was complicated and delayed. During the harvest, there was a lack of workers, ships were late loading, containers were missing, transit time was prolonged, and unloading at the arrival ports was delayed. Shipments that in other years arrived in 2 to 3 weeks, now took 3 to almost 4 weeks. This clearly affected the quality and condition of the fruit that reached the supermarket shelves with problems due to the excessive period of transit. The chains rejected these fruit, diverting it to wholesale markets, and offered at extremely low prices. Added to the logistical and fruit quality problems is the strong increase in supply that is taking place year after year due to the expansion of the crop. The competition between suppliers grows more and more. The largest volumes come to be placed on the market, thanks to the growing interest from consumers around the world. But the great supply has its effect on prices. These are no longer at the attractive values of other years. They are balancing at much lower levels, putting the profitability of more than one company and origin at risk.

CHILE

Chile has managed to establish itself as the leading southern producer and exporter for two decades, being able to overcome all the challenges that arose, both in terms of production, health, and the market. But with the arrival of new players, such as Peru, Mexico and Morocco, the situation for Chile was complicated. These countries have the advantage of having large areas, generally having lower costs and producing blueberries in dry areas, without the incidence of rains or extreme temperatures. While Chile has to deal with frosts, heat spikes, rains during the harvest, as well as a shortage of water for irrigation. There are times when climatic problems affect the quality and condition of the fruits. In contrast, Chile has extensive experience, a good and diversified structure of producing and exporting companies, long commercial relations with importers from the northern markets, commercial advantages thanks to multiple signed agreements and treaties, as well as great government support for sector.

In order to face the growing complexity of the trade, the Chilean blueberry sector decided to devote itself fully to the export of quality fruit, raising the selection standards, limiting the varietal spectrum, towards those that best reach the markets and promoting improvements in the entire string. On the other hand, it fully turned to the production and export of organic blueberries. Frozen food is also becoming increasingly important, a sector in which Chile is the leader in the southern hemisphere.

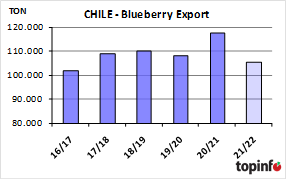

In the current season, efforts to be a quality supplier continued. But the campaign was extremely complex, with blueberries being one of the fruits that suffered the most from the constant delays in shipments. In those that managed to meet the usual times, the blueberries reached the shelves with the quality that characterizes Chilean fruit. But a large part of the shipments suffered constant delays, for which the shipping time went from 2 to 3, 4 and even 5 weeks, which seriously affected the quality and condition of the fruits.

The logistics crisis, added to the strict selection carried out by Chileans, led to export volumes not reaching the levels of previous years. They were around 105,000 tons, which meant 10% less than in 2020/21 and 5% less than the average of the last 5 years. The US was traditionally the main destination, but volumes and its importance within Chilean exports decreased. A few years ago more than 70% went to the US, but in the current campaign it was 51%. Europe was the destination for the volumes that stopped being shipped to North America. Shipments to the old continent are increasing year after year and in this season they received 36% of the total. There were great expectations around the Far East. But progress in this region is complicated and does not show the expected growth. In the 2021/22 season, it received 11% of shipments. In the Far East, the main buyers are China, but also South Korea, Japan and Singapore.

Once again, 15% of the total exported was organic. In this segment, Chile is the absolute leader. It is also in the case of frozen. Given the problems in fresh exports and the minor ones in the US, a higher percentage was allocated to frozen. Also in this case the participation of organic is growing. In 2021 they reached 50,000 tons, of which 72% were conventional and 28% organic.

ARGENTINA

The history of blueberries in Argentina clearly reflects a policy in which the public sector and the social aspect were prioritized before the productive and exporting aspects. In this way a monster state was created that suffocates the productive sector. This was hit hard by the regional economies. The reduction of the orchard area and the drop in exports clearly reflect this lack of understanding. There are many factors that make Argentine fruits less competitive: high internal costs, tax pressure, complex labor legislation, bureaucracy, absence of treaties with purchasing countries, high tariffs, logistical problems, etc.

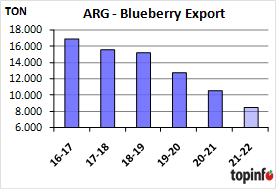

The 2021/22 season ended with an export of 8,500 tons, this is 20% less than in the previous season. Faced with growing competition from other countries, a sharp increase in costs (logistics, supplies, energy) and increasingly complex markets, the Argentine blueberry sector is increasingly concentrating on supplying niche markets. The most important is that of organic fruit, a production regime in which Argentina has long experience and a strong presence in many products. In 2021, 4,083 tons of organic blueberries were exported, therefore almost 50% of the total.

Unlike other competing countries, Argentina has more diversified destinations. Historically, the largest volume was sent to the US, but exports have decreased and currently they receive less than half. In contrast, the participation of Europe is growing. Shipments to this continent have remained in recent years between 3,500-4,000 tons. Although Argentina can send blueberries to China, the volumes are small, given the high tariffs that it has to pay. In the case of organic, it is also Europe that receives the largest volumes. In 2021 it was 66% of the total, followed in importance by the United States. Some goes to Canada, while shipments to Asia remain minimal and punctual.

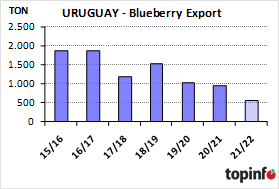

URUGUAY

As in Argentina, also in Uruguay the blueberry business is going through serious difficulties. It spread about 20 years ago at the height of the blueberry boom in the southern regions of South America. In the enthusiasm it was implanted in regions that agro-ecologically were not the most suitable. Given the poor results, these surfaces were soon abandoned, to concentrate production in the Salto region. But also in this area climatic accidents usually happen, such as hail, drought or frost that affect the crop. To which is added high internal costs that remove competitiveness. All this led to a reduction in surface area, production and export. In the 2021 campaign, its export stood at 570 tons, considerably less than in previous years. Of what was exported, 2/3 were sent to the US and the remaining third to Europe.